Debt and Bond Market Crisis

Longview on Friday: “Debt, Reserve Status, and Diverging Bond Markets”

Below is a round-up of Longview related views/research & trade ideas – this is published on Fridays, and updates key themes and highlights key pieces of (often contrarian) research.

By Harry Colvin, Senior Market Strategist, Longview Economics

Key Quotes: “The Threat of Fiscal Dominance”

“[bond markets are] in a fragile place”….“Debt levels are incredibly high — they are ever-increasing”; “While in the past, you might have said, ‘So what? Markets will take it,’ that’s not the case anymore, even in advanced economies.”

Source: International Monetary Fund Deputy Managing Director Gita Gopinath, interview with Bloomberg Surveillance, Thursday 29th August 2025, article available HERE.

“…The US debt problem is the same as the British debt problem before, when the British had a reserve currency, and it’s the same as the Dutch before that - and it’s very basic and very simple to understand”… …“When things become so threatening, then you get a selling of bonds, and you see that reflected in interest rates going up, the currency going down, and the stock market also going down in that dynamic”… “It indicates, right now, when we’re looking at the situation, that we are coming to the end of that long term debt cycle”.

Source: The Master Investor Podcast, 28th July “Ray Dalio: The Risks Are NOT Priced In – Here's What Happens Next”, available HERE.

“We have entered a new era of fiscal dominance”

Source: Kenneth Rogoff, Harvard economist & former Chief Economist of the International Monetary Fund (FT article available HERE)

Chart of the Week: Japanese Long End Yields – New Highs

FIG 1: Japanese government bond yields (10, 30 & 40 year, %)

Bond Market: About to Panic?

Nervousness in the bond market has grown this week, with long end government yields making new highs in several key markets. Yesterday Japanese 30 year yields reached a multi-year closing high (of 3.14%, see FIG 1). Elsewhere UK, German, and French 30 year yields have pushed out to new highs (e.g. see FIGs 2 & 3 below). The US curve has also steepened at the long end, with 30 year yields staying stubbornly high (despite lower/stable 5 & 10 year rates, see FIG 10).

As such, the market chatter has become increasingly bearish, with investors, academics, and commentators starting to worry about a paradigm shift in the global bond market – away from relative stability, and into a ‘crisis phase’.

That is, as the quotes above suggest, debt dynamics have become unsustainable: Interest rates are too high; interest expense will increasingly overwhelm government finances; debt will now accumulate too quickly; and, as such, the bond market has reached its tipping point. In other words, the early stages of a classic ‘debt trap’ scenario are underway, and will be shortly followed by a blow-up in the global bond market.

FIG 2: French 10 & 30 year yields (%)

FIG 3: UK & German 10 & 30 year government yields (%)

The trigger, the bears argue, is Trump’s campaign to reshape (and take control of) the Fed. Arguably that campaign started in early August, with the nomination of Stephen Miran (a White House insider) to the FOMC. That was then followed by the attempt to remove Lisa Cook. All of which is part of a broader effort to bring the FOMC under Trump control (as WSJ’s Nick Timiraos alluded to last weekend – see HERE).

If the government is worried about its own debt dynamics, and sees fiscal dominance1 as the answer, there’s clearly cause for concern. Artificially low interest rates at the front end would, of course, enhance inflation risks. In extremis, the “US debt problem is the same as the British debt problem before, when the British had a reserve currency” as per Ray Dalio’s quote above.

1 when government borrowing needs dictate monetary policy.

Are The Bears Right?

The key question, therefore, is: Are we now in the early stages of that ‘crisis phase’? Is this the end of America’s reserve currency status, as Dalio suggests? How worried should we be? And, why haven’t long end yields broken out to the upside in the US, while other (non-US) yields have moved rapidly higher?

Four key observations are pertinent in that respect:

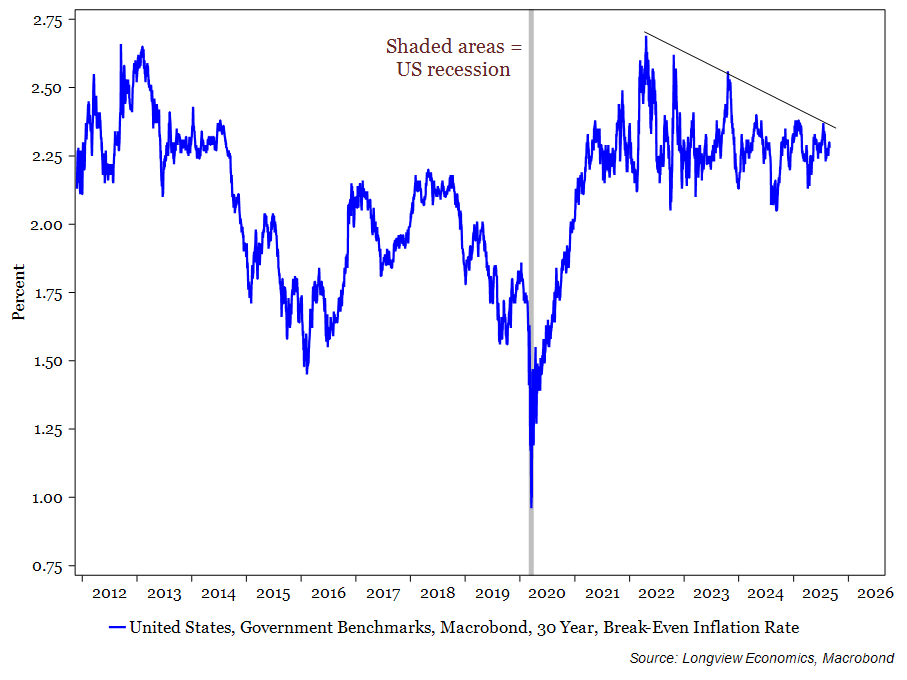

1. While US-related market chatter is bearish/troubling, the Treasury market is behaving well. Unlike Japan, the UK, France, Germany, and others, US 30 year yields remain broadly range bound. With that, 30 year yields haven’t broken out to the upside, closing yesterday at 3.88% (and below their highs from October 2023, of 5.11%), see FIG 10 in the Appendix. In a similar vein, long term US inflation expectations remain contained, with 30 year breakeven rates broadly trending down (FIG 5), while 5 year 5 year inflation is also subdued/stable. Other signs of calm include the ongoing downtrend in US bond volatility (as measured by the MOVE index), as well as evidence of robust liquidity (e.g. measured by the tight spread between ‘on-the-run’ and ‘off-the-run’ Treasury yields2, see FIG 4).

FIG 4: USTs: MOVE index vs. Chicago Fed ‘on the run vs. off the run’ index2

2 The on‑the‑run vs. off‑the‑run Treasury liquidity premium (a Chicago Fed NFCI variable) measures the extra yield required to hold less‑liquid, older 10‑year Treasuries relative to the most‑recent issue (widening spreads indicate reduced liquidity and stress/tighter financial conditions – and vice versa).

FIG 5: US 30 year breakeven inflation (%)

2. The US has the world’s reserve currency status. That explains why the US market is functioning well/remains healthy (point 1), despite having the ‘worst’ debt dynamics of most other major economies.

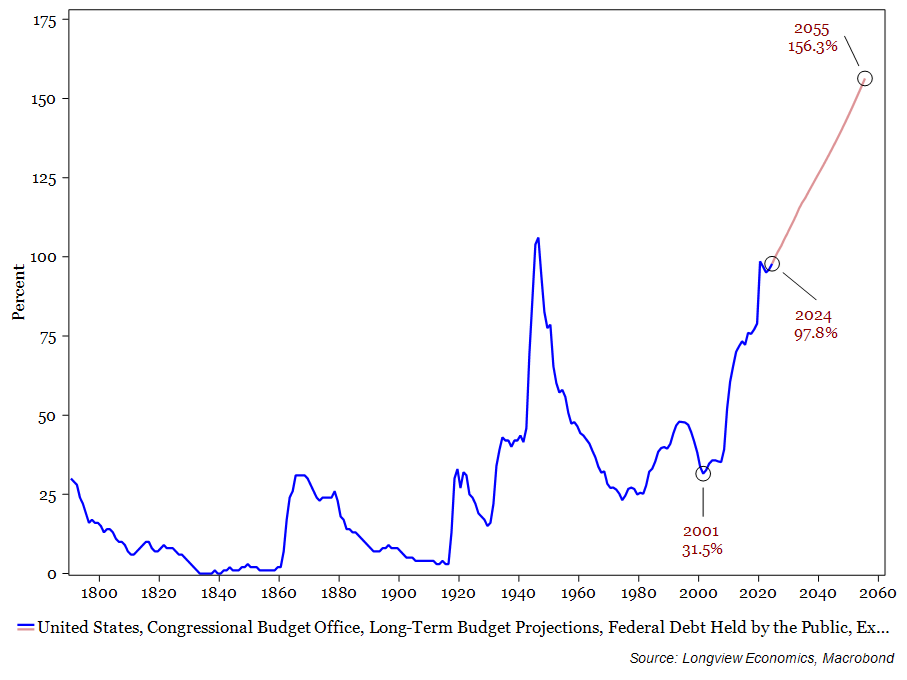

As of December last year, US government debt stood at 121% of GDP (IMF data). That was higher than France (113%), Canada (111%), the UK (101%), and others (albeit not Italy and Japan). More importantly, the increase in US government debt over coming years will be especially fast. On CBO estimates, which are measured differently to the IMF, US government debt will reach 156% of GDP by 2055, up from 98% last year (FIG 6).

FIG 6: US government debt (with CBO forecast), % of GDP

Despite that, reserve status anchors demand for Treasuries, allowing the US to sustain higher debt levels than its peers, while maintaining a low ‘blow up risk’ in the bond market. No other country offers similar levels of liquidity, financial market depth, and institutional strength and trust as the US. With no credible alternative reserve asset (to US Treasuries), therefore, the foreign bid for US Treasuries continues to accelerate (FIG 7).

FIG 7: US Treasury securities held by foreign residents (all countries, USD)

3. If that assessment is correct, then the direction of US Treasury yields should (continue to) be primarily driven by growth and inflation expectations, and less by ‘supply & demand’ factors (e.g. relating to the fiscal balance). In other words, as we highlighted last year, the ‘Wicksellian’ framework is probably the correct one for thinking about the medium term Treasury market outlook:

“there’s a more fundamental approach, which argues that the equilibrium 10 year bond yield is equal to the economy’s trend growth rate (a ‘Wicksellian’ argument). That is, real bond yields are at equilibrium when they trade in line with real trend GDP growth (with inflation added on top to generate an estimate of nominal equilibrium 10 year yields).”

Source: Longview on Friday, 12th January 2024

The US economy, though, remains in the midst of a mid-cycle slowdown, and needs Fed rate cuts/significant policy easing. In that sense, given that inflationary pressures are subdued (see HERE), lower rates are both necessary for the economy and should also ease concerns, at least temporarily, about the emergence of fiscal dominance.

As we highlighted earlier this week, for example, the housing market is unlikely to recover without a marked move lower in long end Treasury yields (and therefore mortgage rates). Without that, house prices would fall further, generate negative wealth effects, and dampen consumption (see HERE for detail). Consumption, though, is the only key driver of US growth currently (with GDP ex. consumption still soft in Q2, even after this week’s upward revisions, see FIG 8).

FIG 8: US GDP excluding consumption (vs. consumption), Y-o-Y %

4. Bond market risks are higher outside the US.

While major central banks are loosening policy, by cutting front end rates, they have also continued to tighten policy by shrinking their balance sheets (i.e. allowing government bonds to ‘run-off’ their balance sheets, in order to unwind/reverse their QE programs). That contraction is happening relative to GDP (e.g. see FIG 9) and in absolute/local currency terms.

For non-US bond markets, which therefore lack reserve currency status, that tightening via the balance sheet drains liquidity in the local bond market. All else equal, that pushes yields higher, especially at longer maturities (which are not pinned lower by policy at the front end). In that respect it’s unsurprising that recent fiscal decisions, to increase the size of the state (e.g. in UK/Germany), are beginning put downward pressure on bond prices (starting at the ultra-long end, where there’s typically less liquidity, and more uncertainty).

FIG 9: Central bank balance sheets (various, % of GDP)

Have a great weekend.

Kind regards,

Harry

Appendix: Miscellaneous charts

FIG 10: US Treasury yields (5, 10, & 30 year yields, %)

Latest Longview Research

This week:

EZ Quarterly Asset Allocation No. 63, 28th August 2025

“Europe: Cyclical Upswing Ongoing” - see HERE

Daily Dose of Macro & Markets:

Daily Dose of Macro & Markets 27th August 2025:

“US Housing: Waiting On The Fed”– see HERE

Daily Dose of Macro & Markets 26th August 2025:

“Liquidity Headwinds!”– see HERE

Weekly Risk Appetite Gauge:

'Weekly Risk Appetite Gauge', 25th August 2025:

“Buyer Exhaustion Creeping In?” – see HERE

Last week:

Longview on Friday, 22nd August 2025:

“AI Capex – How Economically Significant?” – see HERE

Longview Letter No. 150, 21st August 2025:

“Drivers of Global Sector Leadership a.k.a. Sector Rotation - Entering into the ‘Sunlit Uplands’” – see HERE

Longview ‘Tactical’ Alert No. 93, 19th August 2025:

“US Equity Market: Six Warning Signs” - see HERE

Daily Dose of Macro & Markets:

Daily Dose of Macro & Markets 21st August 2025:

“UK Inflation: Under the Bonnet –> Better Than Expected”– see HERE

Daily Dose of Macro & Markets 20th August 2025:

“US Housing Activity: Depressed”– see HERE

Daily Dose of Macro & Markets 19th August 2025:

“Japan’s Nikkei Breakout: Should It Be Chased?”– see HERE

Weekly Risk Appetite Gauge:

'Weekly Risk Appetite Gauge', 18th August 2025:

“The Troubling Message of Volumes” – see HERE